Assessment of the Situation in Türkiye Following the 19 March 2025 Operation

I. Introduction

On 19 March 2025, Istanbul Mayor and Presidential Candidate Ekrem İmamoğlu was detained and subsequently arrested, his diploma was revoked, and his company was seized. This incident was followed by numerous detentions/arrests in the coming days. As of 17 April 2025, it was stated that the capacity of prisons in Türkiye was 300,000; while there were 403,000 detainees and convicts in prisons. The public reacted strongly to the negative developments in the areas of democracy and law, protests became widespread, and calls for early elections began to be voiced across the country. These events caused a significant loss of confidence in the country, leading to a rapid outflow of foreign capital and a shift towards gold and foreign currency domestically. The Central Bank suffered a significant loss of reserves as a result of its foreign currency sales to meet the high demand for foreign currency and prevent the excessive rise in the exchange rate. The policy interest rate, which had been on a downward trend, was raised again to prevent dollarisation and foreign exchange losses. Inflation expectations, negatively affected by the crisis environment created by the 19 March Operation, made the fight against inflation more difficult. In this deepening crisis environment, let us take a closer look at developments in selected indicators.

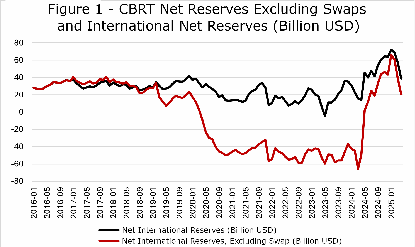

II. Reserve of the Central Bank of the Republic of Türkiye

If we assess the Central Bank's reserves based on ‘Net Reserves Excluding Swaps,’ the item, which bottomed out at minus $65.5 billion in the week of 22 March 2024, entered a strong upward trend following the CBRT's raising of its policy rate from 45% to 50% and completion of local elections on 21 March. During this period, foreign portfolio inflows and the trend towards de-dollarisation among domestic residents provided the central bank with an opportunity to rapidly accumulate reserves. Net reserves excluding swaps peaked at $71.4 billion in the week of 14 February 2025, and dropped to $20.8 billion in the week of 11 April following the 19 March 2025 operation (see Figure 1). In this category, the CBRT's net foreign exchange sales amounted to around $50 billion in the five weeks following the operation. Considering the positive valuation effect on reserves due to the rise in international gold prices, it is understood that net foreign exchange sales were higher. While foreign purchases of equities and bonds played a role in the net reserve increase excluding swaps, alongside entries into the swap market (carry trade), foreign exits from the same investment instruments played a role in the decline. In the four weeks following 19 March 2025, there was a foreign outflow of $1.8 billion in equities and $7.7 billion in bonds. The Central Bank's decision to raise interest rates in April is expected to increase the returns on carry trades. In this case, it is foreseeable that inflows into the swap market (the amount of carry trades) will increase. On the other hand, it can be said that foreigners will be reluctant to take on maturity risk due to the loss of confidence linked to political developments, and therefore investment in long-term bonds in particular will remain weak.

The excessive foreign exchange loss experienced by the Central Bank following the 19 March operation has increased the need for short-term borrowing.

Source: CBRT. Latest data accessed on 18 April 2025.

Short-Term Instruments Used in Borrowing

- Swap – Swap refers to one country exchanging its own currency for another country's currency for a specified period. Swap transactions do not carry currency risk, only interest rate risk. They can also serve a credit function. They can be used to meet temporary liquidity needs. A commitment is made to repay the borrowed amount at maturity with the addition of a pre-determined interest rate. Generally, one of the parties is a reserve currency country. However, in some cases, it can also be done to provide mutual trade and investment financing for the countries party to the agreement. An example of this is the swap agreement made with Kazakhstan on 23 April 2025. The agreement allowed for the exchange of 28 billion Turkish lira or 423 billion Kazakhstani tenge in local currency. The agreement is valid for three years. It may be extended upon maturity. The term of currency swap transactions may be up to 360 days. The minimum transaction amount is 100,000 US dollars or its equivalent in other currencies. As of 29 December 2023, the stock amount of foreign exchange swap transactions carried out by the CBRT is 41 billion US dollars.

- TL-Settled Forward Foreign Exchange Sale Contracts (Non-Deliverable Forward) [NDF] – On the day the NDF agreement is concluded, the parties agree on the forward exchange rate. At maturity, only the profit/loss between the agreed rate and the spot rate on that day is exchanged between the parties. The NDF transaction does not directly affect foreign exchange reserves. Only the exchange rate difference is paid. An NDF is a forward contract used to manage expectations regarding the exchange rate. The maturity can be 1, 3, or 6 months. If the spot rate at maturity is equal to the agreed rate, no cash exchange takes place between the parties. If the agreed rate is below the spot rate at maturity, the difference is paid by the Central Bank to the other party. The Central Bank pays the resulting exchange rate difference by printing money. If the agreed rate is above the spot rate at maturity, the individual pays the difference to the Central Bank. In this latter case, the individual will pay 40 TL for a dollar under the NDF contract, whereas they could have purchased it for 38 TL on the spot market. For every dollar agreed upon, the individual incurs a loss of 2 TL. Therefore, the individual pays the bank 2 TL for each dollar. The instrument can also be considered a type of risk management tool (hedge instrument). NDF was one of the instruments used after the sharp fluctuations in the foreign exchange market following the 19 March operation. Thus, the foreign exchange purchase pressure that the corporate sector could create in the spot market was postponed to a later date, and a possible loss of reserves was prevented because the settlement at maturity was made in TL. NDF is conducted by the Central Bank through an auction method.

- Carry-trade – The carry trade investor carries out this transaction through the swap market. Therefore, carry trade can be considered part of swaps. Carry trade involves borrowing in a currency with a low interest rate, converting the money into the currency of the country where the carry trade will take place at the current exchange rate, and investing it in instruments with relatively high interest rates in that country. Exchange rate stability is important for the return forecast to materialise. Carry trade can also be conducted by Turkish citizens. Carry trade participants earned 34 per cent in dollar terms from Türkiye in 2024. Cumulative carry trade inflows exceeded $31 billion between the 31 March 2024 local elections and 14 February 2025. In fact, due to carry trade, investors are moving away from entrepreneurship and turning to investments such as deposits, bonds and funds.

- FX-Protected Deposit – The FX-Protected Deposit (KKM), used to maintain stability during the crisis that began in 2018, has incurred significant losses to the country. A substantial portion of the 818.2 billion TL loss recorded by the CBRT in 2023 and the 700.4 billion TL loss recorded in 2024 is attributable to the KKM. Peaking at 3.4 trillion TL on 18 August 2023, the KKM has declined to 706 billion TL in the week of 18 April 2025. The accumulation is expected to reach zero by the end of the year.

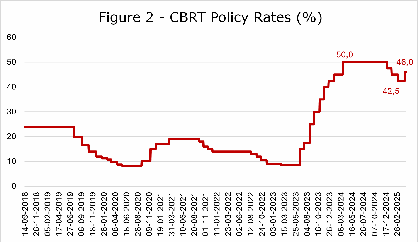

III. Interest Rates

CBRT raised its policy rate by 350 basis points from 42.5 per cent to 46 per cent with its Monetary Policy Committee decision dated 17 April 2025 (see Figure 2). The aim was to prevent a shift towards foreign currency on the one hand, and to encourage short-term foreign currency inflows into the country by increasing carry trade returns on the other. Alongside the policy rate, the overnight rate was raised by 300 basis points to 49 per cent, while the overnight borrowing rate was raised to 44.5 per cent. In parallel, deposit rates for maturities of up to three months rose to 55.7 per cent. Naturally, lending rates have also risen. It is stated that the real cost to a company of a one-year loan with a 55 per cent interest rate and interest payments every three months is over 70 per cent. Had the 19 March operation not taken place, the Central Bank was expected to lower its policy rate from 42.5 per cent to 40 per cent at its 17 April meeting.

Source: CBRT.

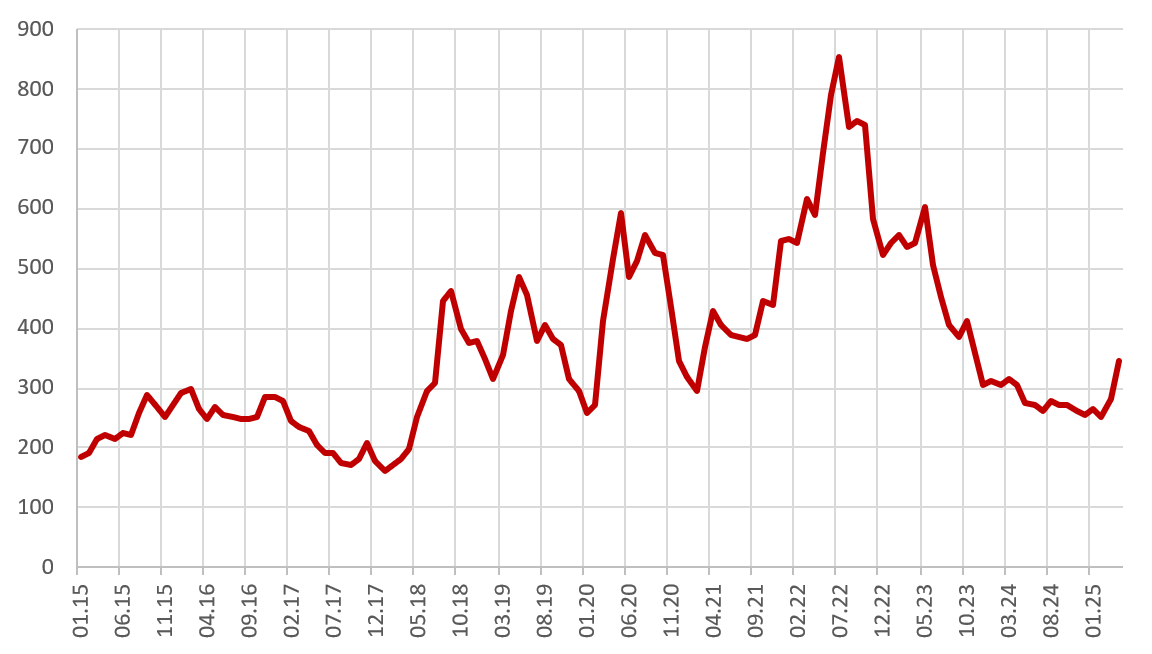

IV. Türkiye’s Credit Default Swap (CDS)

Following the 19 March operation, Türkiye's default swap (5-year CDS) rose from 252 on 18 March to 324 on 21 March. On 7 April 2025, it reached 372 basis points. As of 25 April, the CDS stood at 338.9 basis points.

Figure 3- CDS (5-year, monthly average, basis points)

Source: Bloomberg.

Looking back, the CDS, which had remained below 300 basis points until April 2018, rose above 300 basis points in April as a result of misguided economic policies implemented during the crisis period, reaching over 900 basis points on 14 July 2022. Following the transition to Rational Economic Policy in June 2023, positive developments were observed in the CDS, as in many other indicators. Before the operation, on 19 March 2025, the CDS stood at 271 (see Figure 3).

As is well known, negative domestic and international political developments in a country affect its CDS score. Countries with a CDS above 300 are considered to have highly fragile economies. Indicators of extreme fragility include high borrowing costs, high inflation, high external deficits, weak growth, and excessive dependence on hot money.

V. Inflation

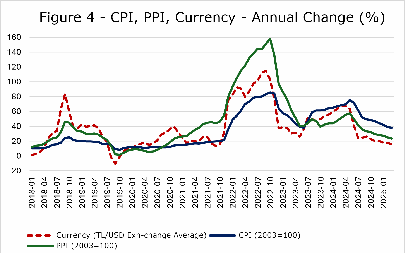

In its Inflation Report dated 2 November 2023, the Central Bank projected inflation rates of 65 per cent for 2023 (forecast range 62-68 per cent), 36 per cent for 2024 (forecast range 30-42 per cent), 14 per cent for 2025, and 9 per cent for 2026. The target for price stability has been set at 5 per cent. However, for various reasons, the targets have not been met, and the Central Bank has often had to raise the target. Although the target has not been met, a disinflation process has begun.

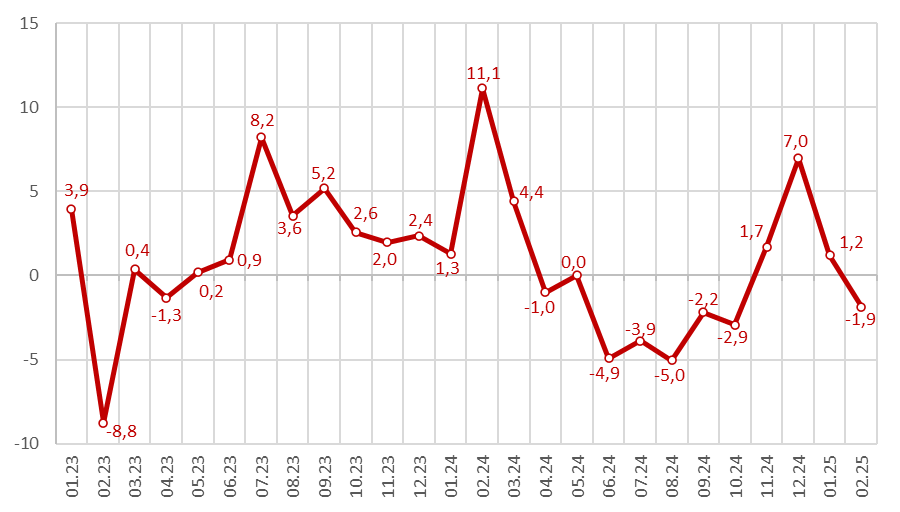

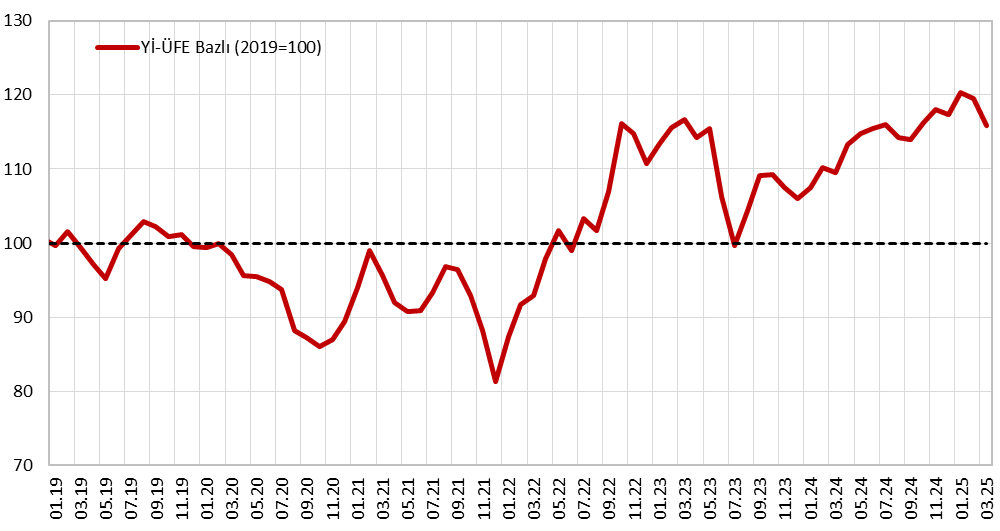

Turkish Statistical Institute (TÜİK) inflation figures show that the Consumer Price Index (CPI) fell from 85.5 per cent in October 2022 to 61.7 per cent in July 2024 and 38 per cent in March 2025. Similarly, the Producer Price Index (PPI) fell from 157 per cent in October 2022 to 41.4 per cent in July 2024 and 23.5 per cent in March 2025 (see Figure 4). It is stated that TÜİK's inflation figures are controversial. Although Inflation Reserach Group (ENAG) and Istanbul Chamber of Commerce report higher inflation figures, the disinflation process can also be observed in their figures.

Source: CBRT, TÜİK. Latest data accessed on 18 April 2025.

For the fight against inflation to be successful, it is crucial that the improving climate of confidence continues. However, the political operation on 19 March had a very negative impact on the process, shaking confidence in many areas.

VI. Industrial Production

According to TÜİK's data, industrial production showed a downward trend from April 2024 to October 2024 compared to the same month of the previous year (see Figure 5). The decline/slowdown in industrial production began to be reflected in GDP growth rates from the second quarter onwards. Indeed, GDP annual growth, which was 5.4 per cent in the first quarter of 2024, was 2.4 per cent in the second quarter, 2.2 per cent in the third quarter, and 3.0 per cent in the fourth quarter. Thus, the Turkish economy, which grew by 5.1 per cent in 2023, slowed down starting from the second quarter of 2024 and ended the year with 3.2 per cent growth. It is expected that the increase in credit interest rates in line with the policy rate hike in April 2025 and the recent increase in global uncertainty due to trade policies will negatively affect industrial production. We anticipate that the slowdown that began in the second quarter of 2024 in Türkiye will continue at a more serious level in 2025. The IMF's growth forecast for 2025 is 2.7%. It has estimated Türkiye’s average growth for the next five years to be 3.4%.

Figure 5– Industrial Production Index

(Calendar-Adjusted, 2021=100, Annual Percentage Change)

Source: TÜİK.

VII. Real Exchange Rate

The dollar exchange rate, which had been at 32 TL following the local elections, has exceeded 38 TL as of April 2025, following a gradual depreciation trend below the monthly inflation rate. As the real exchange rate has not risen in line with the relative purchasing power parity, the TL has become overvalued. The real exchange rate index based on the 2003 base year D-PPI published by the CBRT reached 95.5 in March 2024. When 2019, a period when the current account balance was relatively stable, is taken as the base year, the real exchange rate index is seen to have risen above 100. (Note: The current account balance, calculated on a 12-month cumulative basis, was close to equilibrium in March 2019 with a deficit of $511 million, while it recorded a surplus of $15 billion for 2019 as a whole) (see Figure 6). Under normal circumstances, this would be expected to negatively affect the competitiveness of exports and increase imports. However, the fact that 70 per cent of imports in Türkiye are intermediate goods limits the impact of the overvalued TL. On this matter, the President of the Türkiye Exporters Assembly stated that Türkiye is much more expensive than its competitors worldwide in dollar terms, that exporters have no chance of becoming competitive with incentives, and that Turkish goods remain 20-30 per cent more expensive than those from Asian countries in the US market due to very high costs.

Figure 6 – Real Exchange Rate (D-PPI Based, 2019 = 100)

Source: CBRT. Base year change is the calculation of the author.

The reason for the exchange rate not rising before 19 March 2025 is the abundance of dollars. Hot money entering through carry trade, the conversion of foreign currency deposits into Turkish Lira, and the erosion in the KKM have all contributed to the supply of dollars. This environment has given the Central Bank the opportunity to rebuild its net reserves, excluding swaps, which had fallen to minus $65 billion at the start of the 2018 crisis, following the local elections. In order to prevent the exchange rate increase fuelled by the deepening crisis environment after 19 March, the Central Bank has resumed its intervention in foreign exchange, resulting in a significant loss of reserves (see Figure 1).

VIII. Other Developments After the 19 March Operation

Following the 19 March 2025 operation, alongside the deterioration in financial indicators, Türkiye is experiencing negative developments in other areas as well. Before the wounds of the 2023 earthquake had healed, the 6.2 magnitude earthquake in Istanbul caused great concern, bringing issues such as ‘urban transformation’ and ‘strengthening’ back to the agenda, and the need for financing began to be discussed. The amount of earthquake tax collected over 26 years has reached 145 billion TL. The Special Communication Tax (SCT) was added to the Expenditure Tax Law in 2024, making it permanent. For 26 years, a 10% SCT has been levied on mobile and landline telephone bills, digital and cable TV broadcasts, and internet service bills. The law allowed this money to be used for purposes other than earthquakes. This fund, which was intended to be used for earthquake purposes, was transferred to the Treasury over time and used for roads, personnel expenses, dual carriageways, railways, air transport expenses, education, and payments to farmers. Thus, an important resource for strengthening buildings against a possible earthquake was lost.

The agricultural frost experienced in various regions of Türkiye on 10-11-12 April 2025 negatively impacted production and led to an increase in expectations regarding food inflation.

IX. Conclusion

Following the transition to rational economic policies, positive results had begun to be achieved in the fight against inflation. Inflation had entered a downward trend, CDS had fallen below 300, the country's credit rating had been upgraded, policy rates and other interest rates had begun to fall, confidence in Türkiye had increased, dollarisation had decreased, and Central Bank reserves had risen significantly. The entirely politically motivated operation of 19 March wiped out all these positive developments and caused the crisis in the country to deepen. It is said that policies aimed at stabilising the economy will need to be pursued for 24 months for the economy to regain its balance. The crisis was not limited to the economic and financial spheres; this time, it also caused great trauma in the social sphere. The people who took to the streets demanded only rights, justice and a humane life. If these legitimate demands had been listened to and attempts made to rectify the situation, the country might not have suffered such a deep wound. We hope that common sense will prevail and that the country will return to tranquility as soon as possible. The fight against inflation has become even more difficult in an environment where mistrust is at its peak. The country is struggling to borrow. Even if it can borrow, the cost is very high. The high level of carry trade due to the difference between domestic and foreign interest rates increases the level of risk. Increasing inequality in income distribution, the growing impoverished segment of society, the erosion of trust in the judiciary due to its instrumentalisation, and the deterioration of the country's demographic structure as a result of misguided immigration policies are among the factors contributing to the country's social fragility.

Furthermore, the current inflation control programme has its shortcomings. The production side has not been sufficiently emphasised, and opportunistic pricing has reached high levels due to a lack of oversight. This situation is preventing inflation expectations from being broken. Waste in the public sector cannot be prevented.

In the January-March 2025 period, the central government budget deficit amounted to 710.8 billion TL. Furthermore, the country is under a significant external debt burden. For these reasons, it is in need of affordable credit. There are concerns that rising debt levels and slowing growth could push the country into a debt crisis. Opening up of the credit channels will only be possible if the country does not compromise on fair law.

Although the monetary policy pursued in the fight against inflation is correct, the failure of other relevant units, particularly fiscal policy, to do what is necessary is preventing rapid results in the fight against inflation. In the fight against inflation, all sectors must do their part, waste in the public sector must be prevented, and actions that undermine confidence must be avoided. Maintaining a strong climate of confidence to prevent hot money from fleeing and residents from turning back to foreign currency/gold, providing the necessary support to the agriculture, livestock and industry sectors, and taking the necessary measures to get the economy back on track are just a few of the measures required. More importantly than all of these in the current situation is the immediate elimination of the traces of the political operation created on 19 March. It is impossible to achieve economic recovery in an environment where mayors, party leaders, actors, businesspeople and students are detained.

Note 1: I would like to thank Gülbin Şahinbeyoğlu for her assistance with data collection and graphing, and Çağrı Sarıkaya for his data collection, graphing and constructive criticism.

Note 2: This article has also been published in İktisat ve Toplum Dergisi (Journal of Economics and Society).